From the very beginning of consumer access to home value estimates, WAV Group has echoed concerns about the damage of such a complex and unregulated data point being shared with homeowners. In the housing finance industry, home value estimates are called Automated Valuation Models or AVMs. The models are more of an art than a science – whereby economists handpick a series of data points that get mashed up into an algorithm.

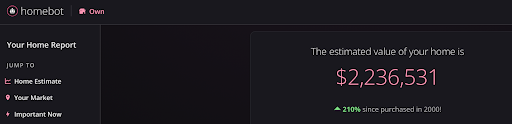

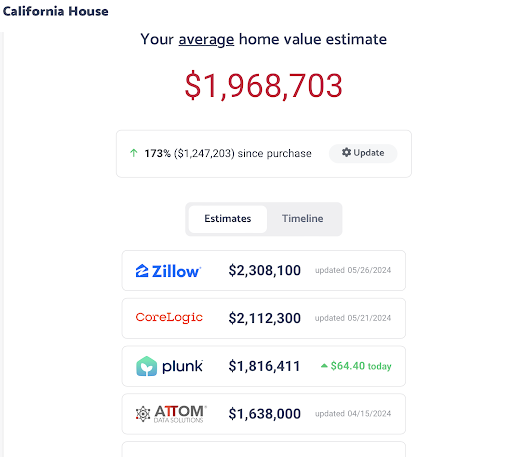

Below is a snapshot of my Homebot valuation, which prompted me to look at other AVMs to compare and contrast the results. The highest valuation was the Zillow Zestimate $2.3 Million. The lowest was Attom Data at $1.6 Million. The difference between the two measuring $700k.

The role of the Consumer Financial Protection Bureau under the Dodd Frank act is to be a watchdog on emerging practices in the consumer financial products or services industry to identify and assess the impact on consumers and other market participants. In June 2023, the CFPB proposed a rule that would regulate the use of algorithms used to appraise the value of a home. At issue is the methodology of the AVMs that cloak the biased inputs in a “false mantle of objectivity.” Sadly, the CFPB proposed rule focused on mortgage originators and secondary market issuers.

Professionals in the real estate industry that help consumers buy and sell homes believe that the CFPB may have looked in the wrong direction. The beauty of the marketplace for professional AVMs used by mortgage originators and the secondary market is that they have access to AVM ratings and experience working with different cascading AVMs. Most importantly, the mortgage industry gets a confidence score on the AVM. Furthermore, mortgage originators are supported by the backdrop of professional appraisers who physically inspect each property. Consumers get none of this detail, they only see a number.

“This discrepancy in AVM data creates a lack of confidence and more confusion to the consumer trying to decide what their options are. This can also make it harder for families to make good financial decisions, when the lack of transparency does not allow for sound decisions and action plans to be followed. In addition, seniors may be more likely taken advantage of by the disconnect on actual value versus a perceived number that may not represent what their true value is”, says Jim Black, Mortgage Loan Officer and Owner of Revest Homes, Inc. NMLS 2362319.

Jim Black, MBA

The Consumer Financial Protection Bureau (CFPB) should evaluate consumer Automated Valuation Models (AVMs) due to their growing influence on the real estate market. AVMs, which use algorithms and vast data sets to estimate property values, can significantly impact consumer decisions regarding buying, selling, or refinancing homes. However, the accuracy and transparency of these valuations are frequently questioned.

Zillow provides accuracy data, but it takes a bit of digging and they only drill down to the county level. There is no city data published by Zillow other than major metropolitan areas. Our county has 94,000 homes. Here is the county data from Zillow.

![]()

Zillow is only within 5% of the property value ⅓ of the time. So that puts my Zestimate in the range of accuracy of $115,000 about ⅓ of the time. Half of the time, the Zestimate is +/- $230,000. Also, 80% of the time, the Zestimate is +/- $460,000. Our county is about 80% farm, and ranch property – a category that the Zestimate has a hard time with. Something like water rights can vary the value of a ranch by millions of $USD. Similarly, a coastal town like Pismo Beach with water views is going to be valued far above a similar community like Atascadero that is 20 miles from the ocean. A city level reporting mandate with published accuracy information would be enormously beneficial to consumers.

Inaccurate AVMs can lead to inflated or deflated property values, causing financial harm to consumers. For instance, an overvalued Zestimate might lead a buyer to overpay for a property, while an undervalued estimate could result in a seller receiving less than their home’s true worth. The CFPB’s evaluation would ensure these models operate fairly, provide accurate estimates, and maintain transparency about their methodologies. By scrutinizing these tools, the CFPB can help protect consumers from potential financial pitfalls and promote a more transparent and reliable real estate market. At a minimum, the CFPB should mandate that all consumer AVMs provide a link to their accuracy data.

Evaluating AVMs aligns with the CFPB’s mission to ensure that consumers are treated fairly and have access to accurate information in financial markets. As these models increasingly influence real estate transactions, it is crucial for regulatory oversight to keep pace with technological advancements. This ensures the protection of consumer interests and the integrity of the housing market.

If you are a broker or Realtor Association that wants to go on the offensive to support consumers, then take action and encourage the CFPB and housing authorities as a consumer advocate.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}